Guest blogger economist Owen Beitsch, PhD, FAICP, CRE, senior director with GAI’s Community Solutions Group (CSG), shares informed analysis of how the percentage of U.S. manufacturing jobs stacks up against those of the nation’s other economic sectors.

The February 2021 jobs report issued by the U.S. Bureau of Labor Statistics indicates that payrolls increased by 379,000 jobs over January 2021, nosing the national unemployment rate down from 6.3% to 6.2%. By far the biggest gains occurred in the leisure and hospitality sector, which represented well over 90% of the jobs added. Manufacturing was also a bright spot, adding about 21,000 jobs.

Manufacturing gains, such as the modest ones experienced in February 2021, generate enthusiastic conversation stemming from the outsized belief that these gains are economically and politically transformative: to wit, former president Trump entered office with the specific claim that he would boost America’s manufacturing capacity and add jobs. His claim was not unusual and aligns with the idea that American wealth is sustained through the power of industrialization.

The past offers an appealing story about American manufacturing. However, our wealth today lies largely elsewhere and vests in very discrete lines of goods-producing activities. While the United States clearly remains the dominant world economy, its employment mix and job concentrations have substantively changed, shifting largely away from goods production to services. According to the St. Louis Federal Reserve Bank, U.S. manufacturing jobs accounted for one-third of total employment in 1945. Today, U.S. manufacturing accounts for only 1 in 12 jobs. Total goods-producing jobs declined from 38 percent in 1945 to just 14 percent of total employment in 2017.

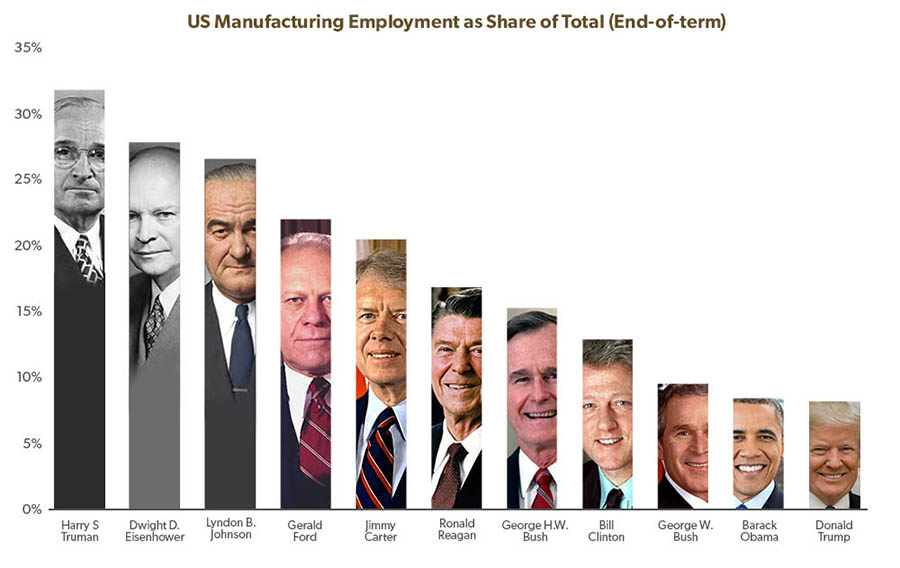

For more than 70 years, every presidential administration—both Republican and Democrat—has ended its term with a smaller manufacturing sector than when it started. Sometimes the total number of manufacturing workers has itself increased, but their share in the total jobs picture has steadily declined. In January 2017, Barack Obama left office with manufacturing jobs accounting for about 8.6% of all jobs. Trump left with the measure at 8.5%, although the decline on his watch may be statistically insignificant and is certainly confounded by COVID-19. Regardless, the movement downward is self-evident and well documented.

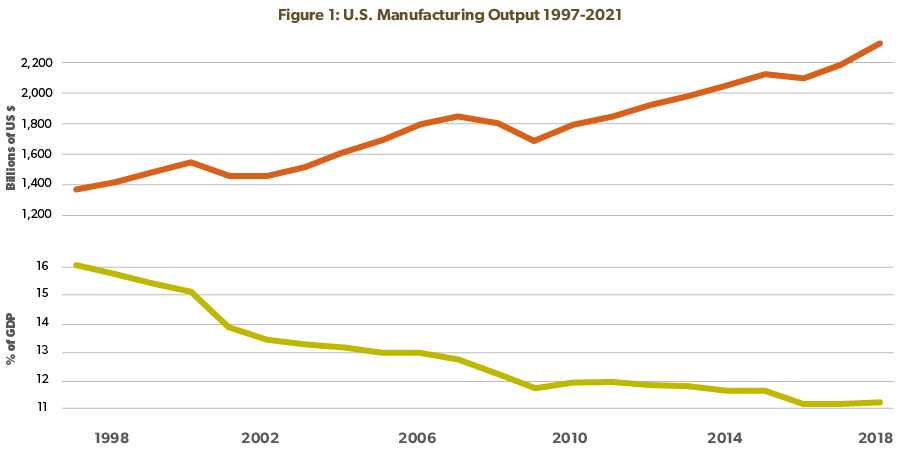

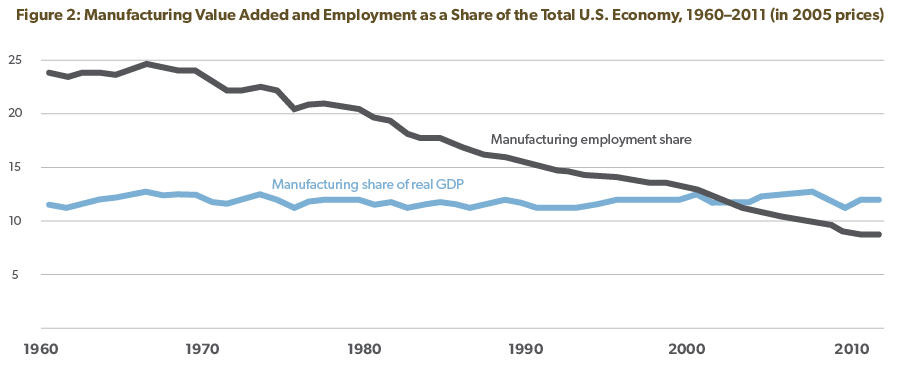

Perhaps more disturbing than the falling number of workers is the falling share of manufacturing as a percentage of the nation’s Gross Domestic Output. Even as the value of manufacturing’s output has increased, its share of the economy continues to drop as shown in both figure 1 and figure 2 below:

An explanation for these trends often centers on trade imbalances and practices, with much of the criticism focused on China’s and other trading partners’ practices and capabilities. In reality, much of what we see in terms of the shift towards the production of services rather than goods began well before China’s rise as a manufacturing economy. Indeed, total U.S. manufacturing jobs peaked nearly 2 decades before the North American Free Trade Agreement.

Like virtually any wealthy, advanced, industrial country, we have a propensity to spend on services and to import more goods than we export, but the explanations for economic shifts are complex. Many variables and trends shape the dimensions of our nation’s resource allocation and capital investment in manufacturing.

- A Shift in Consumer Demand Away from Manufactured Goods

The share of consumer expenditures devoted to manufactured goods has simply declined in the U.S. In 1945, personal expenditures on durable goods accounted for 58% of total spending. Today, consumers spend less than 28% of their expenditures on durable goods. In fact, the content and value of certain items has improved as their cost of production and sale prices have decreased: computers, cameras, televisions, and sound equipment are far less expensive today and vastly superior to earlier technologies and options. We have more but spend less to get it. - Manufacturing Productivity

In advanced stages of industrialization, manufacturers continually invest more capital as manufacturing techniques advance at an exponential pace. Strong growth in productivity—the ability to make more with less—means less employment is required to meet a shrinking consumer demand for durable goods. Robotics will continue to streamline productivity processes and we are witnessing continuous gains where these are deployed. - Changes in the Structure of U.S. Manufacturing Jobs

Goods-producing employers have largely shifted to meeting fluctuations in demand by adding temporary workers, particularly for support functions (e.g., security, janitorial, payroll-processing services, etc.) These structural shifts have had modest effect on manufacturing output, but they do reduce the measured level of employment in the manufacturing sector. - Changes in the Character of Manufacturing

The boundaries defining manufacturing and services have grown fuzzy, especially as more goods [manufacturing] incorporate advanced technology processes [services]. Effectively, jobs that may have previously been deemed manufacturing may be captured in the counts of specialized vendors providing technology and information: does Tesla make cars or promote technology? Should Tesla emphasize the licensing of its technology, it would open the door for other countries to produce and then sell cars based on Tesla’s technical platform. - Disruptions in the Manufacturing Supply Chain

Impacts stemming from supply chain failures are conjectural and not fully understood in the context of the COVID-19 pandemic. Many intermediary products or goods, subsequently necessary to finalize domestic outputs, have not been available upon demand, causing some employment losses. These losses could become permanent if other manufacturing options emerge. Given the relatively low employment counts attributable to manufacturing overall, even modest job losses would be material.

What is the future of America’s manufacturing capacity, its labor needs, and our trade relationships?

Certainly, technology advances are showing themselves to be almost limitless. Even in the midst of the COVID-19 pandemic, the ability to prepare and distribute multiple mRNA vaccines is unprecedented and further underscores the advantages of harnessing new technology to boost manufacturing processes.

Continued advances in technology make it possible for some classes of goods to be manufactured in a variety of settings and locations. Our national employment policies should center on upgrading the skills of its workers to assure they remain relevant. Those skills would be the essential input to more broadly defined manufacturing processes, an approach that builds capacity and labor income without erecting destructive trade and protectionist practices. Classical trade theory speaks to the idea that each country should specialize in the products and crafts it can deliver most effectively and efficiently. For the U.S., that future and specialization seem to vest in services dependent upon enriched skills and knowledge.

To that point, a 2014 study by the Brookings Institute concluded that “the key to expanding U.S. exports and reaching manufacturing’s employment potential is to have companies, domestic and foreign, judge it is profitable to manufacture [in the U.S.].” Policies aimed at strengthening the domestic manufacturing sector can help improve that outlook. However, a move towards protectionism could erase 70 years of economic progress. Little has changed in the last 6 years to alter that view—other than a change in presidential administrations.

Contact Senior Director Owen Beitsch, PhD, FAICP, CRE, 321.319.3131, for more information about the GAI Community Solutions Group’s urban planning, economics, and strategy services. Message GAI online and start the conversation about how our multidiscipline professionals can meet your unique project needs.

Owen Beitsch , PhD, FAICP, CRE has been active in the management and execution of complex studies for public and private clients for many years. His particular interest in special issues confronting urban areas is demonstrated in both his civic and business activities. A member of The Counselors of Real Estate and a Fellow in the American Institute of Certified Planners, Owen concluded several years of service as a member of the Orlando Housing Board of Commissioners. Owen is a faculty member in the urban and regional planning program at the University of Central Florida.

, PhD, FAICP, CRE has been active in the management and execution of complex studies for public and private clients for many years. His particular interest in special issues confronting urban areas is demonstrated in both his civic and business activities. A member of The Counselors of Real Estate and a Fellow in the American Institute of Certified Planners, Owen concluded several years of service as a member of the Orlando Housing Board of Commissioners. Owen is a faculty member in the urban and regional planning program at the University of Central Florida.